government

Health reform after 2014: Not-so-universal coverage

■ About 20 million people are expected to remain uninsured even after the major coverage expansions of the law kick in. Who will these people be?

- WITH THIS STORY:

- » Health coverage carrots and sticks

- » Most remaining uninsured are exempt from mandate

- » External links

- » Related content

The national health system reform law is expected to reduce the nation's uninsured population to what could be an all-time low. But even after the major reforms take effect starting in 2014, millions will remain without coverage, whether by choice or by circumstance.

The health reform law's coverage expansion will vary somewhat by state, but each region of the U.S. is expected to see its uninsured population shrink by roughly half, according to a March 2011 analysis by the Urban Institute, a think tank. About 30 million people are expected to obtain health coverage through private health plans or Medicaid by the end of the decade, leaving about 20 million without coverage.

The Urban Institute study's authors estimated the reform law's impact if it had been implemented in 2011 without adjusting for local health insurance markets, among other factors, so their numbers serve as a guideline, not a prediction. Still, many physicians are likely to see big changes in their patient mixes, according to their estimates.

The health reform law's true impact on the final tally and demographics of the uninsured will be shaped by the decisions of consumers, employers, federal health officials and states. Those who remain uninsured will do so because of such factors as income, insurance costs, employment, legal status and personal choice. Though adding 30 million covered people to the health system over a few years could create many opportunities for doctors to care for more patients, it also could bring unintended problems.

"Anything could happen," said Colin Ford, director of state and federal government relations at the Michigan State Medical Society. "That's just as concerning as having an outcome that we might not like."

Newly covered patients are expected to increase demands for care and prompt greater reliance on physician assistants, nurses and other allied health professionals. That may set the stage for more scope-of-practice conflicts, as nonphysicians assert themselves and physicians continue to resist nonphysician attempts to practice medicine.

"We are extremely concerned about quality of health care delivered under an expansion of the covering of the uninsured," said Gregory Tarasidis, MD, past president of the South Carolina Medical Assn.

Exemption as a factor

The uninsured population was 31 million in 1987 when the U.S. Census Bureau began tracking it. Today it's about 50 million. By 2021, it could drop to 20 million, a level probably not seen since the era of employer-sponsored health insurance began after World War II.

Estimates of this reduction vary. But using their own methodologies, the Congressional Budget Office, the consultant Lewin Group and the Urban Institute predict that the remaining uninsured population will be somewhere between 19.7 million and 23.3 million people.

Part of that population is known already. Many uninsured in 2019 will have some of the same reasons for lacking coverage as uninsured people do today, such as not being legal residents.

"There's absolutely nothing in health reform" for illegal immigrants, said Matthew Buettgens, PhD, a senior research methodologist with the Urban Institute's Health Policy Center and a co-author of the March 2011 study.

Illegal immigrants remain ineligible for Medicaid. The health reform law also prohibits such immigrants -- estimated to be between 4 million and 7 million -- from buying private health coverage in the exchanges, even if they use their own money.

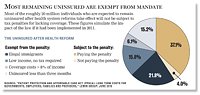

Another mandate exemption will be given to the approximately 3 million nonelderly people earning less than the tax filing threshold -- $9,500 for an individual and $19,000 for couples in 2011.

A few million others will be exempted based on how much insurance would cost relative to their income, or by being uninsured for only a few months, according to the Urban Institute.

Individual factors

The ability of the health reform law's individual insurance mandate to encourage people to stay covered is one major unknown for reform. Nearly 19% of nonelderly Americans are uninsured. The reform law would cut that population to 8.3%, says the Urban Institute study. If just the mandate were taken away, the uninsured population would remain at a relatively high 14.9%.

"You still get a significant increase in coverage through the Medicaid expansion, but you don't see the increase in private coverage you would see with the mandate," Buettgens said.

But people subject to the insurance mandate will weigh the cost of paying the mandate's tax penalty -- which will start as low as $95 for 2014 and increase to at least $695 for 2016 -- with the cost of health coverage, said Jennifer Tolbert, director of state health reform at the Kaiser Family Foundation. Although the penalty will be less than the coverage cost, most people value health insurance, and few will want to pay a penalty and get nothing in return, Tolbert said. Still, a key consideration will be whether the available coverage is affordable for the individual.

The Lewin Group estimates that 7 million might choose to pay a penalty instead of getting coverage, but this is difficult to predict. The Urban Institute model projects that 2.8 million uninsured adults will be subject to the penalty because they will have access to an unsubsidized but affordable health plan. These are expected to be heads of relatively high-income households.

Another difficult prediction is the number of people who will gain Medicaid eligibility in 2014 but remain unenrolled. The Urban Institute projects that about half of those without coverage after the expansion would be eligible for Medicaid but will not sign up. The reform law will remove Medicaid program enrollment barriers, such as in-person visits to caseworkers, paper documentation and detailed financial disclosures, said Buettgens. But even with major efforts to reach out to Medicaid-eligible people, past enrollment rarely has reached 80% of those who qualify.

Employer factors

The health insurance exchanges slated to begin operating in 2014 will serve several functions. They will connect people to new individual and small-group health insurance plans and to Medicaid. They also could offer new choices in group health insurance at a later date.

The reform law pairs these new options with incentives for firms to offer coverage. Employers will not be required to offer health insurance, but certain larger firms will pay penalties if workers obtain subsidized coverage on the exchanges.

The Urban Institute and the CBO suggest that few private employers will discontinue employee coverage because of the reform law. Employers who drop coverage would have to pay higher wages to attract the same employees and would lose health spending tax exemptions. Nondiscrimination laws also prevent employers from dropping benefits only for their lower-income workers, whose wages would be less costly for the companies to boost.

But some observers, such as Paul Fronstin, PhD, director of the health research and education program at the Employee Benefit Research Institute, are skeptical that the national reform law has enough incentives to encourage employers to keep coverage. The Massachusetts health reforms on which the law is based have preserved employer coverage, but the state requires all but the smallest employers to contribute to the cost of employee coverage.

State factors

States already are going their own ways on implementing health insurance exchanges and ensuring that physicians and other health professionals work as effectively as possible. Local decisions by states will impact the number of individuals who remain without coverage -- or who gain coverage but continue to lack access to care.

New Mexico is one state embracing the coverage opportunities under the reform law. The state has one of the highest uninsured rates in the country, which the Urban Institute predicts will decrease by nearly 60% under health reform. The New Mexico Office of Health Care Reform, created in July 2010, is charged with creating a state health insurance exchange to maximize residents' access to health coverage and care, said Dan Derksen, MD, the center's director and former president of the New Mexico Medical Society.

"It's an opportunity for New Mexico to provide health insurance choices based on market principles. We're working full-bore to get that done," Dr. Derksen said. The center also is attempting to improve the state's Medicaid program and its health care work force.

South Carolina's elected state leaders, meanwhile, oppose creating a state insurance exchange, Dr. Tarasidis said. They don't want to make an investment predicated in large part on mandates that could be overturned by the U.S. Supreme Court later this year, he said. Also, state leaders are concerned about the potential cost to them of the law's Medicaid expansion -- another provision the high court could invalidate.

Arkansas' effort to create a local health insurance exchange ended in December 2011 -- at least temporarily -- due to objections from state lawmakers. Arkansas Gov. Mike Beebe instead is focusing on a health care work force group whose initial focus is establishing a medical home program, said David Wroten, executive vice president of the Arkansas Medical Society. The state probably won't be able to train enough health professionals to meet the demand that is expected from reform.

"We are looking at ways of maximizing the resources we already have," Wroten said.

ADDITIONAL INFORMATION

Health coverage carrots and sticks

Click to see data in PDF.

The national health system reform law is expected to reduce the nation's uninsured population by more than half in the next decade. Here's how it aims to do that:

New and expanded coverage

- In 2014, Medicaid eligibility will expand to 133% of the federal poverty level (an effective level of 138%) for nearly everyone except undocumented immigrants.

- Health insurance exchanges will offer plans to individuals and small businesses, later expanding to larger employers at the discretion of states.

- Individuals eligible for exchange coverage who earn between 138% and 400% of the poverty level also could receive federal subsidies to help buy it.

Incentives for individuals

- Most citizens and legal residents will be required to have health coverage beginning Jan. 1, 2014. Most people who remain uninsured face tax penalties, either a set amount or a percentage of income with an annual cap, whichever is higher.

- Exemptions from the penalties will be granted to American Indians, undocumented immigrants, incarcerated individuals, those who remain uninsured for less than three months and people with religious objections.

- The mandate also will not apply to individuals for whom the lowest-cost available plan exceeds 8% of their incomes, and those who aren't required to file tax returns because of their low incomes.

Incentives for employers

- If an employer with 50 or more workers does not offer health coverage, and at least one employee signs up for exchange coverage and obtains a federal subsidy, the employer must pay a penalty based on the number of workers.

- An employer with 50 or more workers that offers coverage would pay a penalty for each worker who instead receives exchange coverage with federal assistance.

- Employers with 25 or fewer employees and with average annual wages of $50,000 or less qualify for tax credits to help them offer coverage.

- Employers with more than 200 employees will be able to enroll their workers automatically, but employees can opt out.

Source: Summary of new health reform law, Kaiser Family Foundation, April 2011